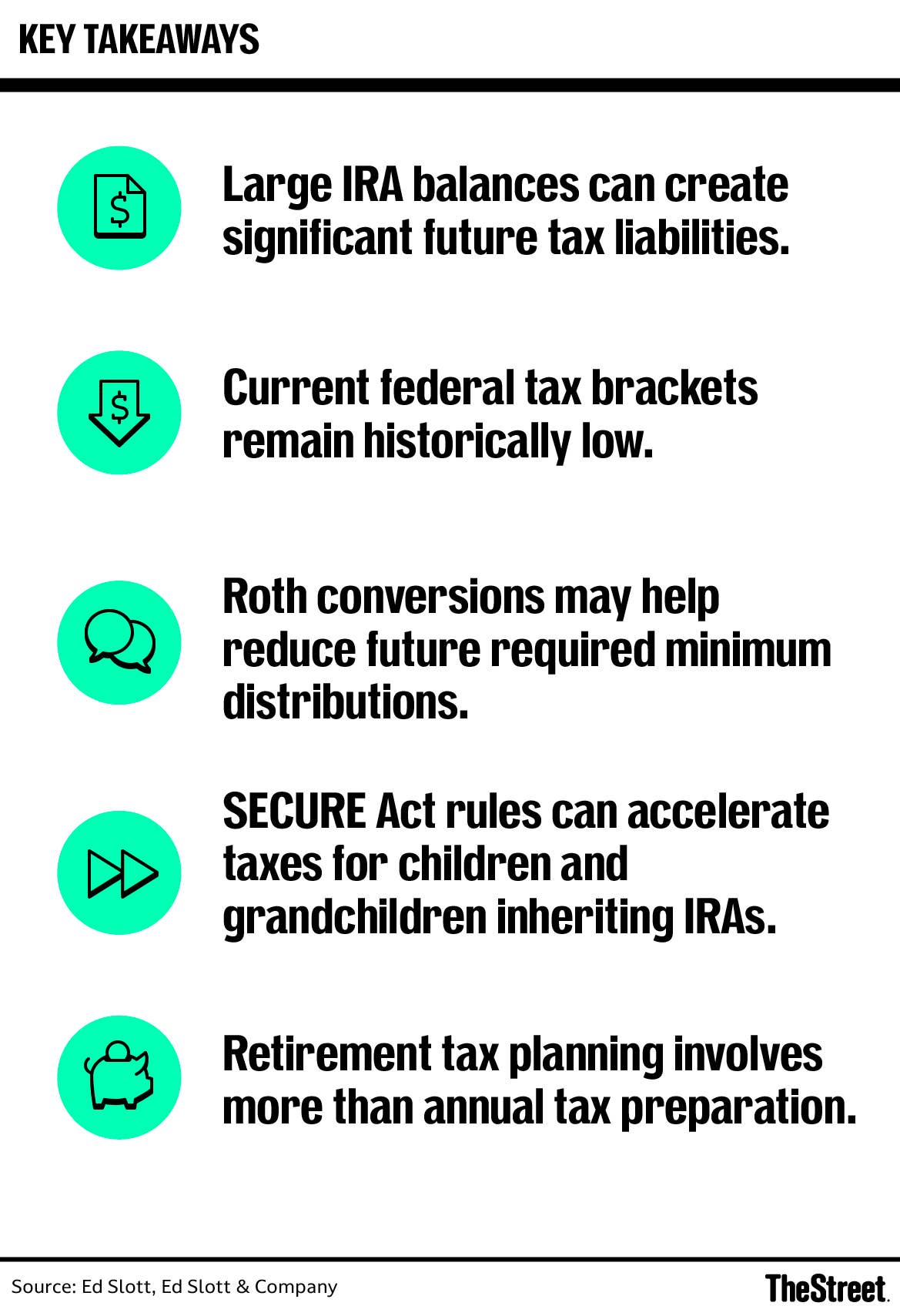

Tax planning for retirement – not just tax preparation – is one of the most underutilized tools available to American savers, yet most financial advisors receive little or no specialized training in it.

At the American College for Financial Services Horizons Conference, retirement planning expert Ed Slott joined Robert Powell to discuss how proactive, lifetime tax planning can permanently lower what retirees and their heirs owe the IRS.

Below is a transcript of the interview with Slott, edited for brevity and clarity.

Tax preparation vs. tax planning

ROBERT POWELL: Ed, you’ll be speaking in a little bit about how proactive planning can permanently lower lifetime taxes.

ED SLOTT: Tax planning is everything. There are a lot of advisors here who do investments, and that’s great – everybody needs to make money. But it’s the second half of the game where all the value is: keeping it and protecting it from taxes, not only today but long-term, lifetime, and beyond – even multi-generational, to beneficiaries.

POWELL: So how do we do that?

SLOTT: Well, first of all, I hate to say it, but advisors have to have the knowledge to do it. Many of them learn all about investing and develop their investing strategies, but very few take any training on tax planning. Some do general tax planning – but not the niche, focused area of tax planning for retirement savings. That’s where all the money in America is, and is going. I don’t know exactly how many trillion dollars are tied up in these accounts – last estimate I saw was $50 trillion. And all of it is going to be taxed.

People are desperate for advisors who have that tax planning knowledge – not just saving your taxes once a year, getting an extra charitable contribution or something, but big-picture tax planning.

POWELL: It’s interesting – CPAs are accustomed to doing tax prep, but maybe not so much tax planning?

SLOTT: Let me say this for consumers who are watching: there is a big difference between tax preparation and tax planning. Tax preparation costs you money. Tax planning makes you money. That’s a big difference.

Why IRA balances are a growing tax risk

POWELL: All right. So I get the knowledge, I find an advisor who has it. What can I expect?

SLOTT: Any advisor worth working with will recognize that after a big market run-up, IRA balances – those tax-deferred accounts that will eventually be taxable – are building up. I hate to say it, but too high. We have more people than ever with a million dollars or more in an IRA. They don’t have any tax-risk diversification. They have all their eggs in one taxable basket.

But something great is also happening. From the One Big Beautiful Bill Act, we have a permanent extension of the reduced tax rates – though we don’t know how permanent that will actually be. Still, we have some of the lowest tax rates in history. So the plan for a good advisor is to find ways to reduce these balances – using Roth conversions, charitable planning, even life insurance – reduce them at historically low rates. Exchanging bad assets for good assets.

POWELL: And people often say it’s important to fill up a bracket with a Roth conversion.

SLOTT: Yes, that’s a key point. You never want to waste a low bracket. Look at these brackets: 10%, 12%, 22%, 24%. These are among the lowest brackets we’ve ever had. And anytime somebody wastes a bracket, it’s gone forever – you never get that back.

Take someone who says, “I’m not going to touch my IRA until I’m 73, RMD age.” Well, that could be 10 years away. Are they going to do nothing for all those years and let the tax bill grow inside their IRA? That’s the problem. Consumers think that money is theirs — but it’s a joint account with the IRS. It’s up to the advisor to say: we have to do something about it. Let’s get these balances down at low rates and build up tax-free to diversify your tax position.

The SECURE Act’s 10-year rule and the beneficiary problem

POWELL: I sometimes think of this as a spreadsheet exercise – a rows-and-columns view showing someone how their tax bill will be reduced over their lifetime by doing these things.

SLOTT: Not only over their lifetime, but for beneficiaries. Remember, the SECURE Act changed everything. Non-spouse beneficiaries – children, grandchildren – are going to get hit at the end of the 10th year after death under the new rules. That’s a 100% required minimum distribution. So if the client’s account is growing and growing, and at the end of 10 years we don’t even know what tax rates will be, we only know what they are now. You can control your tax rates now. You can plan for your lifetime and beyond.

How advisors can build expertise – and how consumers can find them

POWELL: We’ve covered a lot of ground. Anything important we’ve missed for listeners and viewers?

SLOTT: For the financial advisors here, they have to get educated in this. They have to build competence. And the good news is that courses are available – at our organization, at the American College. We have our own two-day program. You’ve been to our elite group program. Once you get educated, it changes you. It builds competence, and competence leads to confidence, and that attracts money.

POWELL: For the consumer who wants to vet an advisor – to know whether they’re dealing with someone who actually has this knowledge – any advice?

SLOTT: This is a little self-serving, but it’s a fair question. We train advisors all over the country, and we list the ones at our highest level – our Elite IRA Advisor Group – on our website under “find an advisor.” They’re not the only qualified people out there, but they’ve committed their time, money, and energy to becoming experts in retirement distribution planning. They know us, and they have us as a back office. That top tier is what we call members of Ed Slott’s Elite IRA Advisor Group. I don’t know of anyone else doing quite what we do in this space.