Stock investors mostly appeared to shrug at last week’s consumer and wholesale inflation reports, which showed steep month-over-month increases, largely due to steep rises in the price of energy products like oil and gasoline.

They finally got the memo on Friday, thanks to a gentle nudge from bond traders.

As the Trump Administration continued pedaling optimism in the Iran negotiation theatre, U.S. Treasury yields broke higher to end last week. That rally in yields, which is tied to the ongoing conflict and inflation, are now pushing a different market to fresh records.

Treasury yields are soaring

On Tuesday, 10-Year, 20-Year, and 30-Year Treasury yields rose to fresh 52-week highs, rising about 3 to 4 basis points each. The 10Y was seen flirting with levels not seen since the inflation scare of the Covid-19 pandemic. Meanwhile, the 20Y and 30Y were surpassed those levels, now at highs not seen since 2007.

That means that long-term yields are now at their highest level since before the financial crisis. What followed was over a decade of low-interest rate policy, marking a sort of generational resurgence in rates.

The increase in Treasury yields is a direct reflection of the unsettle felt in the bond market. While U.S. equities have continued to rally higher on promises for a quick cessation of the ongoing conflict in the Middle East, plus a reopening of important trade passings for energy products, the bond market has finally called the Trump Administration’s bluff.

Their estimation from this vantage point is that rates will rise, not fall.

Rates aren’t going Trump’s way

Many in the bond market had been entranced by promises of lower rates, with the Trump Administration nominating Kevin Warsh to Chair the Federal Reserve. However, with inflation breaking higher, those bets are likely off.

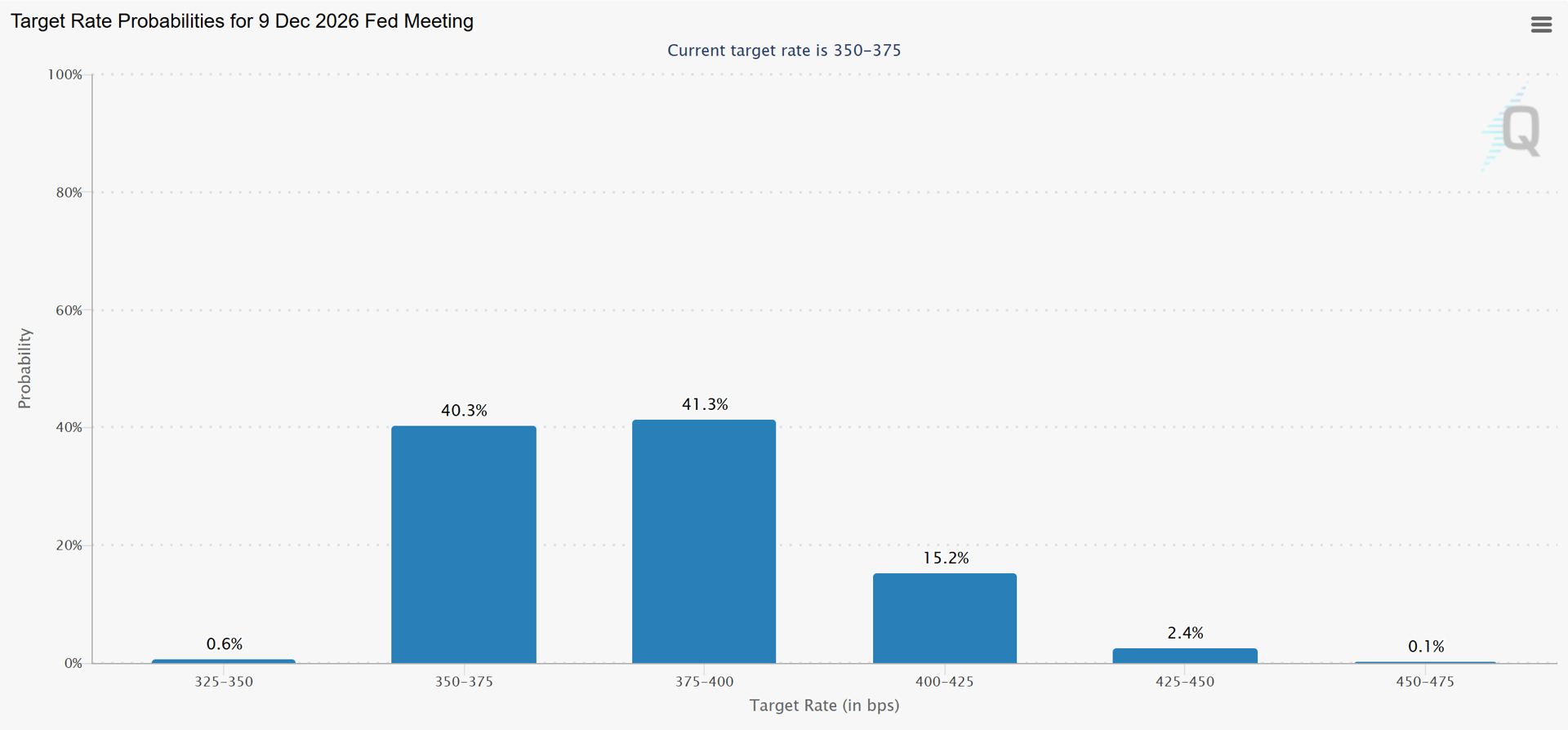

Data from CME Group’s FedWatch show that traders are pricing virtually no rate easing from the current target rate by year-end. Instead, probabilities show that them pricing the opposite: a 59.1% probability of a rate hike.

With cuts more or less precluded, traders are positioning themselves accordingly. Bank of America’s latest global fund manager survey says that 62% of respondents are now betting on the U.S. 30-year to surpass 6% assuming there is a “big move in yields over the next 12 months.”

Bad for the economy, bad for the market

Rates at these levels bare huge consequences for the U.S. economy and the stock market. If they rise even further, it could be seriously detrimental for both the economy and a significant portion of the market.

On the economic side, higher yields increase lending rates. This affects consumers through higher borrowing rates for mortgages, vehicles, and other lines of credit. It also affects businesses, particularly smaller ones, which are reliant on floating rate debt.

The stock market is currently beginning to process this. While many large companies are immune from large debt sales, small- and mid-cap businesses reliant on floating rate debt are likely to be adversely affected. Companies in the Russell 2000, many of which are unprofitable, are likely to be punished by ascendent rates.

In fact, an increase in rates could derail an impressive comeback rally in the Russell, which has gained nearly 30.7% on the year, even accounting for the recent declines.

What happens next?

At the start of 2026, investors bet the bank on rates falling, bolstering asset valuations. Jerome Powell and the Federal Reserve had more or less delivered the soft landing. The ongoing conflict in Iran throws a wrench in that.

Perhaps if the bond market no longer faces illusions about the precarious state of the conflict, it stands that the stock market might be made to join in that realization. With over a month of assurances that a deal with Iran is coming and little fruit, the market might be on thin ice.

During this time, the Strait of Hormuz has remained shut. So long as it does, supply chain disruptions only worsen. Energy prices, which have contributed the most to the uptick in inflation, are advancing higher after weeks of relative calm. Continuous Contracts in Brent Crude Oil were little-changed Tuesday, but now sits at $111, closer to the top of the 52-week range. U.S. oil prices are only a few bucks cheaper.

How does this compare to Covid?

It stands to reason that if oil prices drop, inflation will drop too. This is an overly simplistic consideration of the current environment, as energy costs are passed along for all other goods.

However, for us to toil with the issue of how the knock-on effects of this exogenic oil shock would affect the prices of goods and services in the broader economy, we’d have to know when the war will end. And as it stands, the Strait of Hormuz is still closed.

Many big bank analysts had banked on a resolution to the conflict by Summer, but Summer is at the doorstep, and the Strait is still shut. This amounts to the largest disruption to the oil market ever; a matter worsened by each day that it remains shut.

It’s impossible to predict the tides of war, nor when a breakthrough might come, but those expecting a soft-landing scenario like the one coming out of the Covid-19 pandemic are likely to be disappointed. Sure, they both bare resemblance to each other in some ways, but we are in considerably worse shape this time.

The U.S. economy was in the enviable position of having printed trillions in stimulus to cover for the chaos. When inflation did rise, the economy had boast worthy levels of employment and wages for many Americans kept pace or exceeded the rate of inflation. This is unlikely to be the case today.