That roar you keep hearing?

It’s not a World Cup crowd.

Those cheers are coming from investors and consumers after a stunning drop in consumer prices in June that appears to put the kibosh on an anticipated interest-rate hike later this month.

So what’s the Federal Reserve’s next move?

The U.S. central bank still has to wade through wobbly oil prices, sticky inflation, the artificial intelligence buildout, and a potential new round of tariffs for the rest of the year, even after June Headline CPI dropped to 3.4% month over month from May’s 4.2% figure. Core inflation stayed flat.

Improvement in headline inflation reflects the drop in oil prices that followed the signing of the U.S.-Iran Memorandum of Understanding, said Ebury Head of Market Strategy Matthew Ryan.

“We’re not yet seeing elevated energy prices feed into second-round inflation pressures,” he added in an email to TheStreet. “We’d caution against reading the data as the start of a clean, linear path to target given the changing energy backdrop, though this is an encouraging sign of disinflationnonetheless.’’

Ryan added that if Iran-U.S. peace talks deteriorate, “a September hike is very much back in play.”

Futures traders see a 83% probability that the Federal Open Market Committee will hold interest rates steady at its rate-setting meeting July 28-29. The CME Group FedWatch Tool is also forecasting a near 63% probability of a rate hike at the FOMC September meeting.

Warsh skirts interest-rate outlook on Capitol Hill

Kevin Warsh made his first appearance as Fed Chairman before the House Financial Services Committee just a few hours after the better-than-expected CPI read dropped.

Warsh acknowledged the Fed has “more work to do” on inflation but avoided signaling the direction in which the 12-member FOMC is leaning.

“While monthly price fluctuations are inevitable — especially in an unsettled world —underlying inflation over longer time horizons is determined largely by monetary policy,’’ Warsh said in his prepared remarks.

Warsh commits to “price stability“

Warsh was delivering the Fed’s twice-yearly Monetary Policy Report to Congress. He appears before the Senate Banking Committee June 15.

The report, issued July 10, said the outlook of the future path of interest rates “is subject to considerable uncertainty.”

It also described the U.S. economy as overall “expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East.’’

Warsh repeatedly reminded House members that the Fed is committed to its dual Congressional mandate: use interest rates and balance-sheet policy to keep prices stable and the labor market at full employment.

That’s tricky.

- Lower interest rates support hiring but can fuel inflation. This risks fueling further inflation, potentially leading to an inflationary spiral.

- Higher rates cool prices but can weaken the job market. This increases the cost of borrowing and further stifles economic activity.

Warsh repeated his pledge that the central bank would work on its “resolute commitment” to restore price stability.

Fed holds interest rates steady

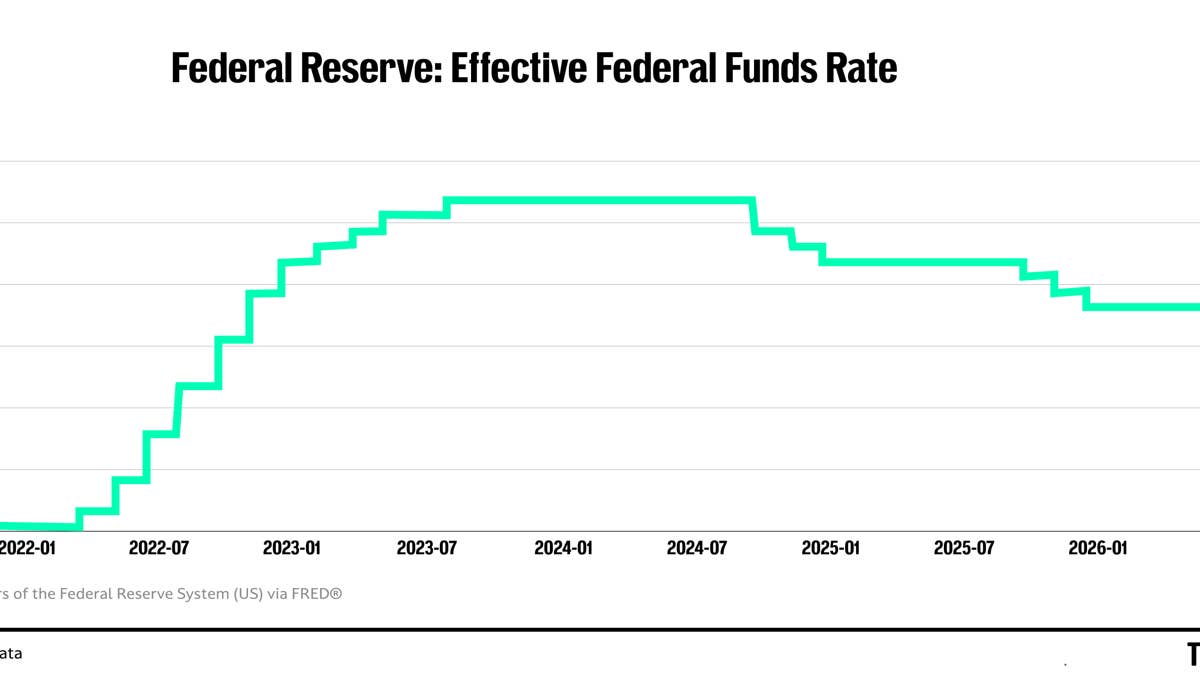

The rate-setting Federal Open Market Committee voted unanimously last month to hold its benchmark Federal Funds Rate target in a range of 3.5% to 3.75%.

But the minutes of the June FOMC meeting showed policymakers split on inflation risk and the impact on interest rates.

The funds rate is the interest rate at which banks lend balances at the Federal Reserve to other banks overnight. A change in the funds rate triggers moves in borrowing costs ranging from credit cards to auto loans to even mortgage terms.

Related: Fed’s Warsh faces tough interest-rate smackdown in Congress

Policymakers had cut rates by a quarter point at each of their last three meetings of 2025 to shore up the softening labor market.

These “insurance” cuts stopped after the majority of policymakers decided the risk from higher prices outweighed signs that the jobs market was stabilizing.

Warsh focuses on Fed “regime change,” inflation

In a note to clients, economists at Evercore ISI said the “very benign June CPI inflation report gets Warsh off the hook in terms of pressure to hike near-term and allows him to position the Fed as resolutely committed to bringing inflation back to target without fueling expectations of a July move.”

The last time year-over-year inflation was at or below the Fed’s 2.0% target was February 2021.

“If we get policy right — and we will — the inflation surge of the last five years will be a thing of the past,” Warsh said.

Long-term inflation a major concern

Although the cooler CPI is pricing out a July rate hike, Fifth Third Commercial Bank Chief Economist Bill Adams said longer-run inflationary pressures persist. These include labor shortages in industries with high shares of immigrant workers, including nursing and home health care, as well as sustained higher prices, fueled by climate change, for foods such as beef and veal.

“The Fed will need to see more good news on inflation to hold off on interest-rate hikes in the rest of the year,’’ Adams said in an email to TheStreet.

Related: Fed’s Waller issues stark warning on inflation, interest rates