How Trumpy will it be?

Now that Kevin Warsh’s nomination as the next Federal Reserve Chair blasted through a few roadblocks, the Senate Banking Committee is expected to approve the former Fed Governor’s nomination April 29.

Then the GOP-controlled full Senate is expected to confirm President Donald Trump’s nominee in time for him to assume the role when Jerome Powell’s term as chair ends May 15.

The president made it very clear throughout the monthslong process of naming a replacement for Powell that he would only nominate a candidate who agreed with his monetary policy stance.

While Trump said earlier this month that he would be very disappointed if Warsh did not begin to cut interest rates immediately, he also said has not discussed rates with him.

Analysts believe an independent central bank anchors inflation expectations, boosts investor confidence, and supports stable economic growth by insulating monetary policy from short-term political pressures.

Investors are reassessing Warsh’s potential impact on markets and Fed independence after the Justice Department dropped its criminal probe into Powell, an unprecedented investigation seen by Powell himself and many economic and financial leaders as an attempt by President Trump to bully the Fed into slashing rates.

“There is, of course, what Kevin Warsh would like to change versus what ultimately the market will allow him to change,’’ Michael Kramer of Mott Capital Management told Seeking Alpha.

Warsh calls for “regime change” at Fed

Warsh testified repeatedly during his confirmation hearing April 21 that he would maintain Fed independence from executive authority.

He also called for a “regime change” at the central bank that includes:

- Dropping the quarterly “dot plot” which shows Federal Open Market Committee member expectations for short-, intermediate-, and long-term economic projections.

- Fewer press conferences and speeches by Fed officials on economic conditions and interest-rate outlooks.

- Changing the Fed’s preferred inflation metric — the core PCE — to remove the biggest outliers and reflect a “trimmed mean” number, which would lower the actual inflation rate.

- Shrinking the Fed’s $6.6 trillion balance sheetso that it has a less dominant impact on markets and relies less on quantitative easing.

Iran war impacts Fed future rate bets

At the start of the year, when Warsh’s nomination was made public, GDP was set to get a boost from deficit-financed fiscal stimulus and more Fed rate cuts, according to Moody’s Analytics Chief Economist Mark Zandi.

“Job growth would resume, and unemployment would stabilize. Hard to see this happening now,’’ Zandi said in a LinkedIn post.

“Even if the Iran War winds down and oil prices recede quickly, the fallout will ensure there is no GDP pickup or job growth this year. Unemployment will rise further, and already considerable recession risks will worsen.”

More Federal Reserve:

In the eight weeks since the Iran war began, the United States is the only country not facing severe supply chain disruptions that prompt shortages and trigger much higher recession risks.

Yet higher prices at gas pumps across America are just one sign that the war’s impact is being felt by consumers, investors, and businesses here.

Yes, there’s even been buzz about Fed rate hikes

KMPG Chief Economist Diane Swonk said in a LinkedIn post that there is no easy or clear path ahead for the Fed.

She called inflation “a regressive tax. It spurs inequality & compounds over time, leaving the level of prices too high for too many.”

Related: Investors question Warsh’s future impact on markets

“There is not one but many reasons for what we are enduring but only one institution devoted to rectifying it — the Fed. Coming close doesn’t count in central banking,” Swonk said.

“Further muddying the waters for the Fed are the war, continued uncertainty about tariffs and how innovations in AI could impact the economy in the near- and long-term,’’ she said, adding that as a result, some Fed officials are “weighing a hike as well as cut,’’ she added.

How markets are viewing Fed independence under Warsh

Markets are less focused on Warsh alone and more on how long he can resist White House pressure.

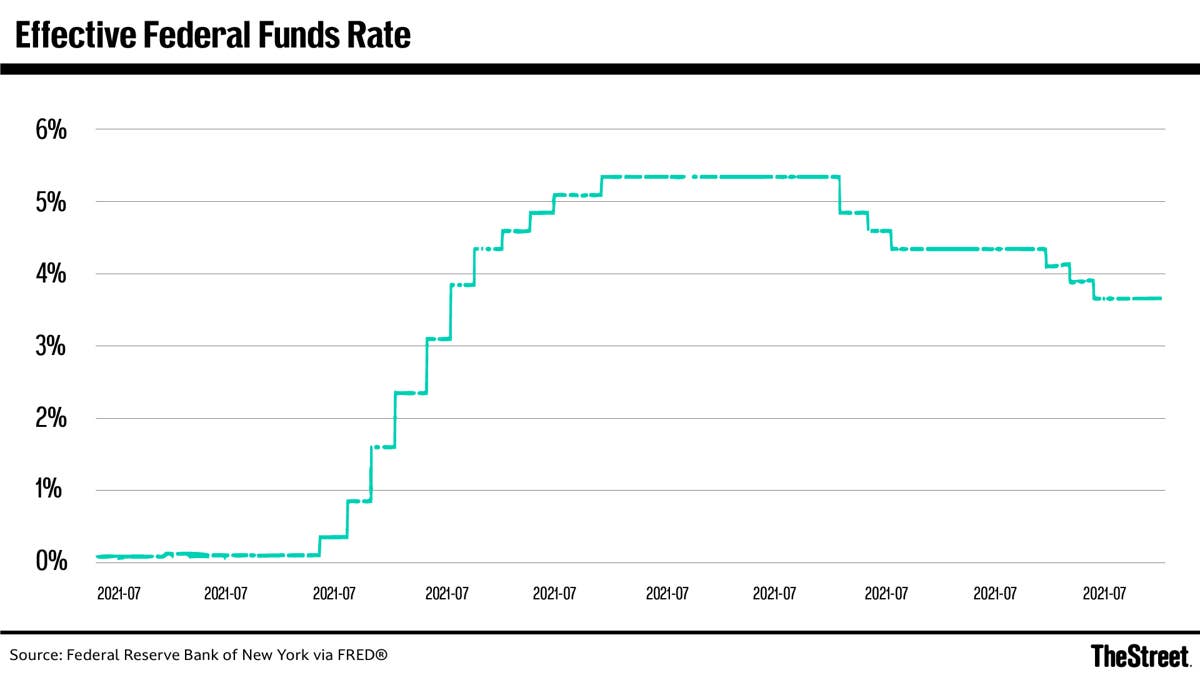

Right now, the CME Group FedWatch Tool is pricing in the next Fed rate cut for late 2027, not the immediate rate cuts President Trump has demanded.

This is a noticeable push out from earlier this year, which saw at least two quarter-point cuts in late 2026. The FOMC April 29 meeting is widely expected to hold rates steady at 3.50% to 3.75%.

But there is also increasing belief across Wall Street that institutional constraints, including the fact that Warsh is one of 12 voters on the policy-setting FOMC, will outweigh Trump’s influence.

The Fed’s congressional mandate calls for maximum employment and stable prices. The Fed regional bank presidents, including the FOMC voting members, have been more vocal in recent months about inflation than the labor market.

Investors eye Warsh’s plan to shrink Fed balance sheet

Kramer of Mott Capital said Warsh’s plan to shrink the balance sheet could be the most critical of his desired changes.

“We know that the Fed is already operating close to the lower bound of ample reserves, as seen in funding market behavior in late 2025, when SOFR became more volatile and usage of the standing repo facility increased,’’ Kramer said.

“It suggests there is limited room to further reduce the balance sheet without destabilizing funding markets. In that sense, the constraint on Warsh’s changes may not come from the Fed itself, but from the market,’’ he said.

Related: Markets question Powell’s future after DOJ drops probe