The Federal Reserve’s divisive vote to hold interest rates steady March 18 underscores the central tension now driving U.S. monetary policy.

Investors are no longer debating whether risks to the Fed’s dual mandate exist, but which risk matters more to the U.S. economy.

On one side, inflation remains stubborn. Producer prices came in hotter than expected March 18, showing acceleration that began before the Iran war began.

The risk? Inflation could reaccelerate rather than continue its slow drift toward the Fed’s 2% target.

In addition, economic drive is also showing signs of weakness. The softening labor market and slowing growth would typically prompt interest-rate cuts.

This was a path markets had been expecting just a few weeks ago.

The Iran war, by driving energy costs sharply higher, has reopened the traditional stagflationdilemma of rising prices with slowing growth.

The stagflation fear helps to explain not only the Federal Open Market Committee’s decision to hold the benchmark federal funds rate at 3.50% to 3.75%, but also the divided vote.

“Whenever you have the Fed’s dual mandate become a dueling mandate, there should be debate,” Diane Swonk, chief economist at KPMG, told Bloomberg before the Fed announcement. “And the reality is that we don’t have the luxury of other central banks of just looking through the inflation, given that we’re five years in and the risks of it becoming more entrenched rise by the day.”

Another looming risk: an interest-rate hike that is starting to gain voices, due to concern over current macro and geopolitical views of the economy.

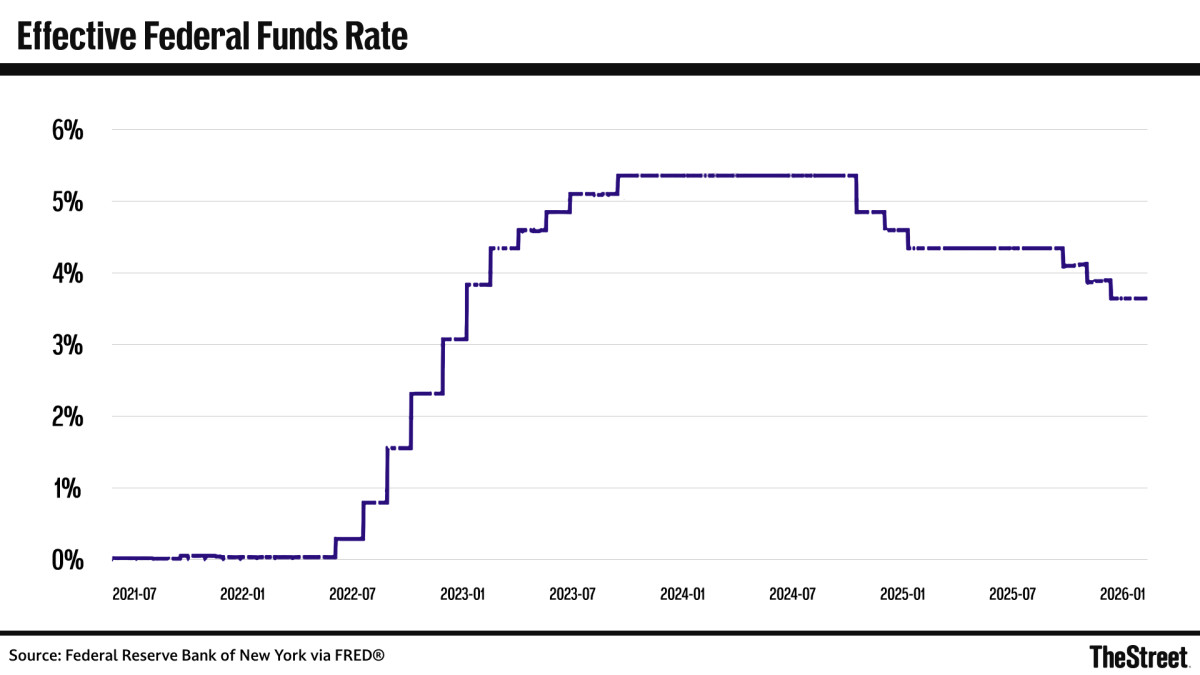

FOMC votes 11-1 to hold rates steady

The FOMC voted 11-1 to continue to pause benchmark interest rates.

Fed Governor Stephen Miran, who has advocated for multiple rate cuts since joining the board in September, dissented in favor of a quarter-point cut.

In its press release, the FOMC said available indicators suggest that economic activity has been expanding at a solid pace.

It noted that “job gains have remained low, and the unemployment rate has been little changed in recent months. Inflation remains somewhat elevated.

“Uncertainty about the economic outlook remains elevated. The implications of developments in the Middle East for the U.S. economy are uncertain,’’ the release also said. “The Committee is attentive to the risks to both sides of its dual mandate.”

Federal Reserve Bank of New York via FRED®

What the Fed’s dual mandate requires for jobs, prices

The Fed’s dual congressional mandate requires it to balance full employment and price stability.

- Lower interest rates support hiring but can fuel inflation.

- Higher rates cool prices but can weaken the job market.

The two goals often conflict, operate on different timelines and are influenced by unpredictable global events like pandemics and wars.

More Federal Reserve:

Even before the outbreak of the Iran war, the Fed faced a dilemma from worrisome risks to both sides of its congressional mandate: higher unemployment rates and sticky inflation.

Prior to the release of the latest inflation and GDP figures for January and February, Fed officials displayed a divisive outlook on 2026 interest-rate cuts.

How the federal funds rate affects you

The benchmark federal funds rate impacts nearly all Americans.

That’s because it guides interest rates for auto and student loans, home-equity loans, and credit cards.

It also impacts the 10-year Treasury bond, which in turn affects mortgage rates in the stagnant housing market.

Billions of dollars in taxpayer money — primarily from individual tax returns and payroll taxes — pay the interest on the nation’s $38.9 trillion debt.

For consumers, a delayed rate cut could mean higher borrowing costs during an affordability crisis, causing many Americans to scramble to pay energy, grocery, shelter and health care bills in a “low-hire, low-fire” labor market.

FOMC also paused rate cuts in January

The FOMC voted 10-2 to hold interest rates steady at 3.50% to 3.75% in January after three consecutive quarter-point cuts in its last three meetings of 2025.

Those cuts were based on data showing increasing weakening in the labor market and cooling inflation, although still sticky and tariff-laced.

Fed Chair Jerome Powell told reporters after the December 2025 meeting that the economy was settling into a neutral range.

A neutral range for economists means monetary policy is neither stimulating nor restricting economic growth.

It was the FOMC’s first pause since July 2025.

Fed releases latest “dot plot”

The Fed’s “Summary of Economic Projections” provides its estimates of inflation, unemployment, and economic output, in addition to estimates of interest rates that officials see as most appropriate policy over a three-year horizon.

The interest rate estimates, also known as the Fed’s “dot plot,” are closely watched on Wall Street for insight into the central bank’s thinking and plans.

The SEP is a quarterly report from all 19 Fed officials, including the 12 voting members of the FOMC.

It measures several key economic variables including:

- Real Gross Domestic Product growth: Recently revised GDP came in at 0.7% for Q4 2025, a sharp slowdown from 4.4% growth in Q3 2025.

- Unemployment rate: This was recently reported higher than expected at 4.4%, following a disappointing February payroll report.

- Inflation: Includes both projections for Personal Consumption Expenditures (PCE) inflation and core PCE inflation excluding food and energy. January PCE came in at 2.9% year over year, above the Fed’s 2% annual target.

The March “dot plot” calls for a single rate cut in 2026, the same as the December 2025 forecast.

This breaking news story will be updated.