When you’re 10 years away from retirement, it’s not quite time to start a countdown. After all, you still have 120 months to go until your time in the labor force is over. Still, now’s a good time to make sure you’re on track for a secure retirement and address any savings gap that may have you worried. Here are some key moves to make when retirement is 10 years out.

Related: Retirement Countdown: Key moves to make when you’re 30 years away

Play catch-up in your retirement account

Once you turn 50, you’re allowed to start making catch-up contributions in your IRA or 401(k) plan. And it pays to make them if you can swing them, whether you’re “behind” on retirement savings or not, since that money gets tax-advantaged treatment.

If you’re using an IRA to save for retirement, this year’s catch-up contribution is worth $1,100, bringing your total allowable 2026 contribution to $8,600.

If you’re using a 401(k) plan to save for retirement, the catch-up rules are a bit trickier (but not necessarily in a bad way). For one thing, 401(k) catch-ups have a much larger value. The general catch-up limit is $8,000, bringing your total allowable contribution to $32,500.

However, if you’re between the ages of 60 and 63, there’s a super catch-up available to you worth $11,250. That brings your total 2026 contribution up to $35,750. You should also know that thanks to a new rule, if you earn $150,000 or more, any 401(k) catch-up you make has to be in a Roth account.

Now if you’re in a position where you’re able to max out a 401(k), including a catch-up, then chances are, this change applies to you. However, it’s a common strategy for people who mainly have traditional IRAs or 401(k)s to start Roth conversions in the years leading up to retirement. So by being forced to make catch-ups in a Roth 401(k), you’re basically just getting the ball rolling early.

Read: The reverse mortgage as a retirement lifeline

Reassess your portfolio’s risk profile

When you’re 20 or 30 years away from retirement, you can afford to take on plenty of risk in your portfolio. But with only 10 years ahead of you, it’s time to start thinking about preserving your savings and protecting yourself from a market crash and/or a forced early retirement.

To that end, review your asset allocation and aim to start shifting away from stocks – but only just a bit. Remember, you still have a good 10 years ahead of you to ride out market volatility.

What you may want to do is limit your stock market exposure to 70% to 80% of your total assets, depending on your risk tolerance, this year. Then, over the next 10 years, you can gradually scale back until you have more of a 60%/40% split between stocks and bonds, or whatever split makes you comfortable.

You may also decide to reduce your exposure to stocks more substantially if you’ve saved a lot and want peace of mind during your final decade in the workforce.

Imagine you’ve saved $3 million to date and have a goal of retiring with $5 million. If you contribute $30,000 toward your savings over the next 10 years but also scale back on stocks so that your portfolio is generating a 5% yearly return, you could end up over $5.2 million even with a conservative asset allocation.

Look into long-term care insurance

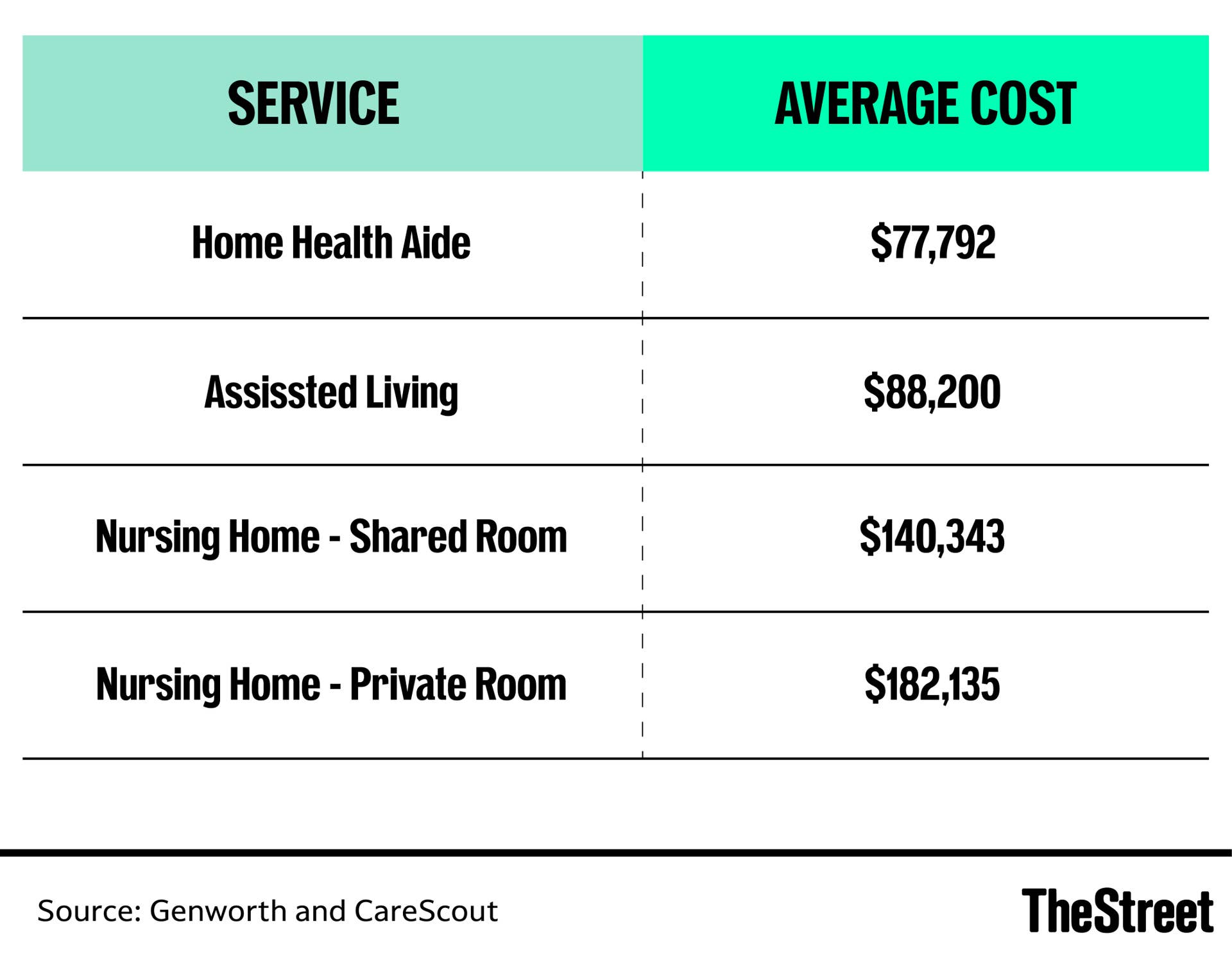

Healthcare costs are one of the largest unknowns in retirement. While Medicare covers many medical expenses starting at age 65, it does not typically cover long-term custodial care. This means that if you end up needing a home health aide, assisted living, or nursing home care, you may have to foot the bill entirely on your own.

That bill may be larger than expected, though. Here’s what long-term care costs, on average, on a national scale:

That’s why it’s a good idea to look into long-term care insurance, which, depending on your coverage and needs, could largely pick up the tab for services like these.

Long-term care policies vary widely in terms of coverage, benefit periods, and premiums. But generally, premiums are lower when you apply in your 50s or early 60s.

When evaluating different long-term care policies, don’t just focus on premium costs. Also look closely at:

- Benefit limits

- Benefit periods

- Waiting periods

- Inflation protection riders

If you decide not to buy long-term care insurance, you could instead “self insure,” which basically means saving money to pay the full cost of long-term care yourself. But it’s important to have a plan one way or another.

Tackle your remaining debt

Entering retirement with significant debt could strain your budget and cause you a lot of stress. So it’s best to kick off retirement debt-free if possible, and now’s the time to start working toward that goal.

Start by listing your outstanding debts in order of costliest interest rate to least costly. And then reassess your near-term spending to free up money to pay them off. Not everyone manages to go into retirement mortgage-free, and that’s okay. But try to shed high-interest debt like credit card balances before your career wraps up so you’re not saddled with monthly payments to make on top of your other expenses.

If you truly have a lot of debt, one thing you may want to consider is consolidating it into a single loan. If you have a lot of home equity and are still paying off your house, a cash-out refinance could be a reasonable solution if you have good credit and can therefore qualify for a competitive interest rate.

With 10 years of work ahead of you, retirement may seem like it’s still a ways off. But the moves you make now could make a huge difference in your retirement lifestyle.

So to recap:

- Make catch-up contributions in your retirement accounts if you can swing them.

- Reevaluate your portfolio setup.

- Look into long-term care insurance.

- Work on shedding debt, especially the costly kind.

By taking action, you can move closer to retirement with more confidence.

This series on retirement produced for TheStreet by Nifty 50+