TheS&P 500 has been churning between 6700 and 7000 since November, but under the surface, there’s been a major shift in winners and losers.

It’s no longer big-cap technology that’s delivering mouth-watering gains. Instead, it’s baskets like energy, consumer staples, and healthcare that are winning – a worrisome trend given those sectors tend to perform best in the late stages of the economic cycle.

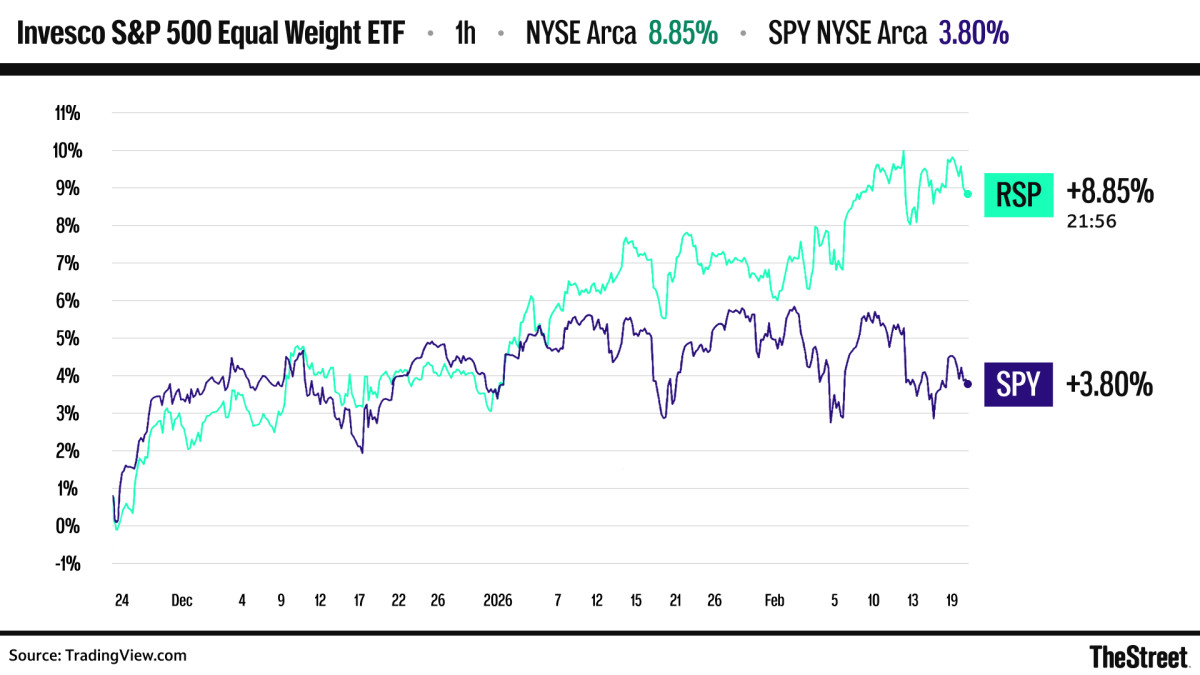

Those groups, plus utilities (XLU), which just shot up Limelight Alpha’s sector ranking, are racking up big gains – a seismic shift that has led to index ETFs that more closely track them, including the Russell 2000 and equal-weight S&P 500 (RSP), to outperform.

The magnificent seven is far from magnificent this year, with the average member slipping 7% year-to-date, and the Roundhill Magnificent Seven ETF tumbling 12% from its peak last fall and flirting with a loss of technical support at its closely watched 200-day moving average.

The shift in performance has sparked debate over whether the technology slide is a pause that refreshes or a harbinger of more losses.

L

Sector model pivot sends cautionary message on what’s next

Limelight Alpha’s multi-factor sector model crunches data weekly to rank baskets more or less likely to reward investors. The ranking, based on my research from the early 2000s when I was working on Wall Street’s sell side, has confirmed energy stocks’ dominance since last fall, when rattling sabers raised the possibility of unlocking Venezuela’s massive oil reserves.

Related: Analyst resets Chevron stock price target as oil strategy shifts

The ranking has also pivoted to reflect ongoing interest in diversifying away from technology, which has scored below average for weeks, toward previously under-loved groups, including healthcare, basic materials, and staples.

Now, Limelight Alpha’s latest weekly data has added another defensive twist: utilities, a favorite basket among defensive-minded investors, has surged into the second spot in the large-cap ranking, trailing only energy.

|

Large Cap |

|

|

Average Score |

|

|

ENERGY |

82.83 |

|

UTILITIES |

81.67 |

|

BASIC MATERIALS |

74 |

|

CONSUMER GOODS |

72.68 |

|

INDUSTRIALS |

72.16 |

|

HEALTHCARE |

69.64 |

|

FINANCIALS |

66.19 |

|

REITS |

62.2 |

|

SERVICES |

61.35 |

|

TECHNOLOGY |

59.23 |

|

Source: Limelight Alpha |

The pivot isn’t a call to change long-term investment plans. However, it is a signal that should remind investors that stocks don’t go up (or down) in a straight line. Instead, they zig and zag, with many pops and drops along the way, creating risk and opportunities for investors.

What’s driving the shift from technology to defensive sectors

It’s certainly possible that the weakness in technology stocks is simply a speed bump along the way to greater gains down the road.

There’s a good argument that February’s market churn is to be expected, given seasonality suggests February is traditionally a weak link, including during mid-term election years. I wrote more about February being a ‘banana peel’ month here.

It’s not lost on me that we also saw similar doubts hit technology stocks last year, when questions emerged about massive AI spending plans derailing corporate profits. Most stocks recovered strongly through last fall, before struggling.

Instead of a wholesale S&P 500 sell signal, sector rotation may simply reflect a transition to a more discriminating investor as AI interest shifts from “anything at any price” to a focus on who the real winners and losers are.

That would certainly seem to be true based on the performance of software stocks, which have tumbled this year amid fear that agentic AI would dismantle software-as-a-service as we know it, crimping sales and profit growth, and forcing a rerating after years of a higher-than-market valuation driven by the industry’s sky-high margins.

With technology, arguably priced to perfection, including software stocks, accounting for over one-third of the S&P 500, it’s not out of bounds to expect a mindset shift to “prove it” that would lead to erasing some stock market froth.

And then, when you consider companies more likely to benefit from such a shift, defensive groups like energy, healthcare, consumer staples (and yes, utilities) do fit the bill:

- These companies are traditionally weighed down by hefty, fixed costs that AI may conceivably reduce, boosting margins and earnings while technology margins get squeezed by rapidly rising spending plans.

- Utilities stocks are likely to benefit from rising energy demand from all those power-hungry server farms coming online and lower interest rates’ impact on interest expense.

- Healthcare, utilities, and staples stocks tend to perform best in the late stage of the economic cycle, when GDP growth is peaking, and the risk of deceleration emerges, increasing risk-off appetite.

What can investors do now?

The S&P 500 has successfully held around 6750 to 6800 since November. If that changes, then we could see a more substantial retreat toward the 200-day moving average, which rests currently near 6500.

Long-term investors have historically been rewarded for dollar-cost averaging into market weakness, but short-term investors may want to rethink their exposure, especially if they’re using leverage like margin, which can worsen losses.

If this is simply a February swoon, the market should start to head higher soon. The Stock Trader’s Almanac reviewed all mid-term election years since 1949, and typical February weakness tends to end by early March, with the S&P 500 trending up through mid-April before sliding again through summer ahead of the election.

If it’s a signal of something worse, investors will want to keep a close eye on how the S&P 500 behaves if it fails to eclipse 7,000, falls, and retreats to the 200-dma.

In any case, building small starter positions in those defensive sectors, including utilities, may help you diversify some risk if you’re overly exposed to tech stocks.

Overall, if you zoom out, there is some good news: While 2026 appears to be volatile, mid-term weakness has historically presented an intriguing buying opportunity.

“Where there is great danger, there is also great opportunity,” wrote Stock Trader’s Almanac’s Jeffrey Hirsch. “After reaching negative territory in Q2 and Q3 stocks should rally in Q4.”

Related: $386B fund manager sends strong Europe, US stocks message