Time was when having health insurance and being financially protected from healthcare costs were the same thing.

That’s no longer the case according to a new report, the Employee Benefit Research Institute (EBRI)/Greenwald Research Consumer Engagement in Health Care Survey.

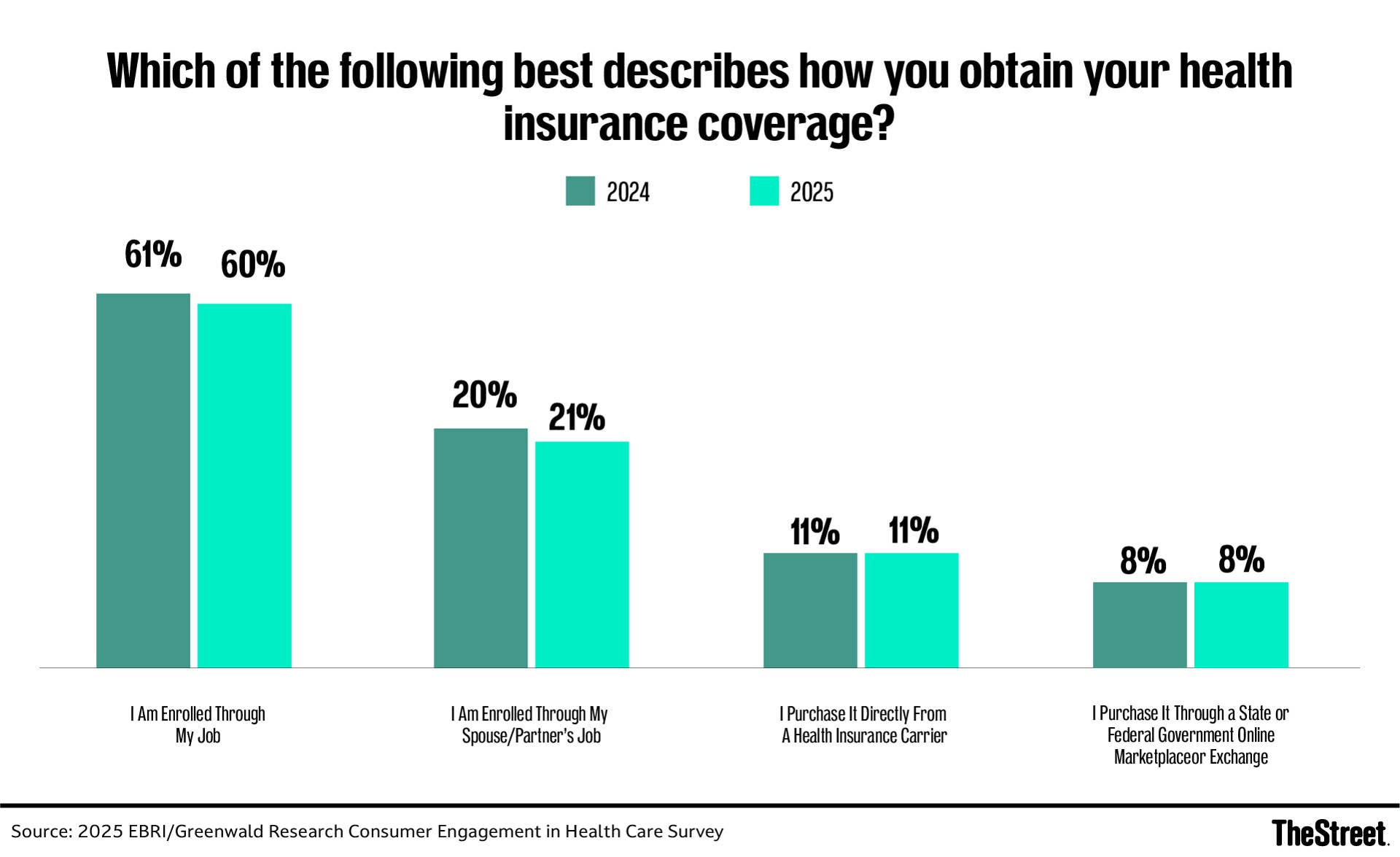

The survey found that employer-sponsored coverage still dominates, with roughly six in 10 insured individuals receiving coverage through their own employer. But the more significant shift may be this: deductibles have become nearly unavoidable, even in plans that historically shielded workers from major upfront costs.

In effect, many Americans still have insurance, but they are increasingly responsible for absorbing thousands of dollars in healthcare costs before coverage meaningfully begins.

Among the findings:

- More than three-quarters of insured workers now have a deductible.

Even among traditional plan enrollees, 70% now face deductibles.

The share of traditional-plan participants with deductibles rose from 65% to 70% in just one year.

The shift is forcing workers to think less like passive insurance buyers and more like financial risk managers.

Here’s what experts say workers should consider.

Don’t evaluate plans based solely on premiums

Monthly premiums remain the number many workers focus on during open enrollment. Financial planners say that’s often a mistake.

Robert Biesiada, certified financial planner with Revolve Wealth Partners, said medical utilization should usually drive the analysis.

“If you are an individual that is primarily only seeing medical professionals for preventive care and minor illnesses, a high deductible health plan may make a lot of sense,” Biesiada said.

He said many high-deductible health plans carry lower premiums than traditional copay plans, and the gap can widen further when employer HSA contributions and tax savings are factored in.

“The lower premiums and potential access to a health savings account may significantly offset the higher deductibles,” he said.

Even households with higher medical costs may benefit in some cases “if the premiums and HSA savings offset the deductibles enough,” he said.

Michael Angell, associate professor at the College for Financial Planning – a Kaplan Company, said age and family size should also shape plan selection.

“Age is a major factor,” Angell said. “A typical 20-year-old generally has different health care needs than a typical 50-year-old.”

Younger workers may be able to tolerate higher deductibles and lower premiums. That equation changes as healthcare utilization rises later in life.

Family structure matters too.

“Statistically, a family of five is more likely to incur medical expenses than a single individual,” Angell said.

He also said some couples unnecessarily duplicate coverage by both enrolling in employer-sponsored plans.

“This can be an unnecessary expense, as one policy is often sufficient to cover the family’s needs,” Angell said.

Deductibles aren’t the only number that matters

Experts say workers should evaluate deductibles, out-of-pocket maximums, provider networks, prescription drug costs and employer HSA contributions together, not separately.

Expected healthcare usage is often the best starting point.

“They should all be reviewed in conjunction with your personal situation,” Biesiada said. “Expected utilization is likely the best starting point.”

Workers also need to assess whether they could realistically absorb a large medical bill if the worst happens.

“A positive cash flow or ample rainy/sick day fund could allow a buffer for higher than expected medical care,” Biesiada said.

For some households, predictability matters more than minimizing premiums.

“Some folks are choosing to pay higher pretax premiums for copay-type plans for the predictable copays,” he said.

Angell said one of the biggest mistakes consumers make is choosing the lowest-premium option without preparing for the deductible exposure that comes with it.

“A common mistake consumers make is choosing the lowest-premium health plan and simply hoping for the best,” Angell said.

That can become financially dangerous when a major illness or hospitalization occurs.

“When a serious medical event occurs, they are unable to pay those out-of-pocket costs and often turn to high-interest credit cards,” Angell said. “This can begin a downward spiral of unmanageable debt.”

Stress-test the worst-case year

The experts said workers should stop assuming healthcare costs will remain stable from year to year.

Instead, households should model what a bad healthcare year would actually look like financially.

Biesiada said workers should begin with their own medical history and anticipated care needs.

“Workers should take their personal healthcare history and upcoming care as the guideline as to which plan option may be suitable,” he said.

He also noted that workers can typically reevaluate coverage annually during open enrollment if their needs change.

Angell offered a simple benchmark for financial preparedness.

“Here is a simple test: if you do not have enough money in your HSA to cover your full deductible, your HSA is underfunded,” he said.

Without that reserve, workers may be forced to tap retirement accounts or accumulate high-interest debt during a medical emergency.

“Without a fully funded HSA, you will most likely be forced to rely on savings, credit cards, or retirement accounts during a medical emergency,” Angell said.

He noted that while some 401(k) withdrawals for medical expenses may avoid early-withdrawal penalties, they generally remain taxable as ordinary income.

Rising deductibles are changing consumer behavior

Higher deductibles are also changing how workers use healthcare.

“Folks are more aware of potential higher costs and changing their behaviors on how they access care,” Biesiada said.

Telehealth usage has increased partly because of lower costs, he said, and workers are paying closer attention to provider networks.

“People are also being very mindful of staying in-network to keep their costs lower,” he said.

Angell said advisers are seeing some workers delay or avoid care because they fear the financial consequences of using their insurance.

“Yes, advisers do see this happen,” Angell said.

He said middle-class households often face the greatest pressure because they may not qualify for public assistance yet still lack sufficient reserves to comfortably absorb large deductibles.

“Many middle-class households … are caught in a difficult position: too affluent to qualify for assistance, yet without enough financial reserves to comfortably absorb significant out-of-pocket medical costs,” Angell said.

Open enrollment mistakes can become expensive

Workers also make avoidable mistakes during open enrollment.

One common error, Biesiada said, is assuming the most expensive plan automatically provides the best protection.

“Depending on their needs, they may be paying very high costs for benefits they are not utilizing,” he said.

Families may also overlook more cost-effective ways to split coverage between spouses.

“It may make sense for one employee to stay on a plan by themselves while the other covers the dependents,” Biesiada said. “A family plan may not be the most cost effective.”

Angell said another overlooked gap is disability insurance.

“One common mistake workers make during open enrollment is failing to also enroll in disability insurance coverage,” he said.

Health insurance may pay medical bills, he noted, but it does not replace lost income if an illness or injury prevents someone from working.

The broader financial lesson

The experts said rising deductibles strengthen the case for larger emergency reserves, more disciplined HSA funding and more conservative assumptions about healthcare costs before Medicare eligibility.

Biesiada said healthcare costs continue rising across the board.

“Premiums, deductibles, and maximum out-of-pocket limits have steadily gone up,” he said.

Angell said HSAs remain one of the most tax-efficient savings tools available.

“Perhaps the best-kept secret about HSAs is that balances can be carried into retirement and used to help cover Medicare out-of-pocket expenses,” he said.

Among the recurring recommendations from advisers:

- Fully fund an HSA whenever possible

- Maintain at least three to six months of emergency savings

- Compare total potential annual healthcare costs, not just premiums

- Reevaluate expected healthcare utilization annually

- Consider disability insurance during open enrollment

- Pay close attention to provider networks and out-of-pocket maximums