When I bought a home in 2022, housing prices were skyrocketing. I was panicking, and so were my fellow hopeful homebuyers.

On the other hand, home sellers were thriving as they were selling their houses for way more than they had paid originally. Homeowners were approved for high-dollar-amount second mortgages or cash-out refinances.

Over my years of reporting on the housing market, I’ve learned that although home price trends impact everyone in the real estate market, there’s no scenario that benefits everyone.

All ears perk up when there are new predictions about the future of home price growth, because they know it will affect them. As a homeowner, I’m as curious as everyone else.

The government-sponsored enterprise (GSE) Fannie Mae has released its Q2 2026 Home Price Expectations Survey, which breaks down panelists’ projections for the next few years.

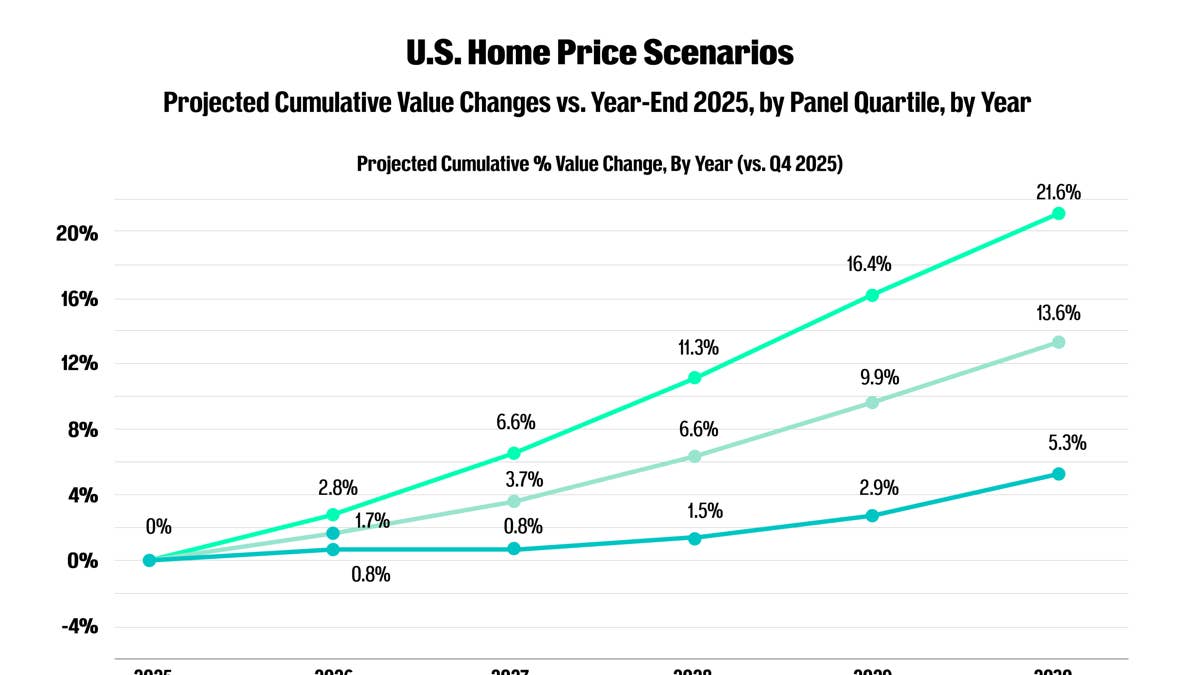

Fannie Mae panelists’ average expectations are for housing prices to increase by 1.7% in 2026, 2% in 2027, and 2.8% in 2028. It’s important to remember these numbers, but there’s much more to their predictions than these three percentages.

Fannie Mae home price predictions through 2030

Home prices can decrease in extreme markets, such as the housing bubble bust between Q4 2006 and Q1 2012. And costs might decrease for a few quarters in a local real estate market. But, in general, homes prices increase.

Those inclines are more like spikes in major seller’s markets. For example, Fannie Mae data shows that prices jumped by 7.8% during the housing bubble (Q1 2000-Q3 2026) and during what it calls the “Covid Reshuffling” period (Q2 2020-Q1 2026).

Housing prices don’t always increase this aggressively, though. In fact, it isn’t the norm at all. And starting in Q2 2026, many Fannie Mae panelists expect price growth to calm down.

Related: More on housing prices

Fannie Mae releases data from the panel’s optimists, those who expect prices to rise faster, and the pessimists, who project slower growth. Then, it combines all responses to produce the panel-wide numbers.

Between Q4 2025 and Q4 2030, the panel-wide expectation is for home prices to increase by 13.6%.

Overall, the panel projects an average annual price increase of 2.6%. The Fannie Mae Home Price Index (HPI) shows that yearly home price growth has been gradually slowing since Q1 2024, with a Q1 2026 growth rate of 2.8%. This means the GSE expects annual growth to continue cooling.

Home sales impact housing prices

When home-buying demand increases, house prices generally rise in tandem. The opposite is also true: When demand decreases, prices remain stagnant or even decline.

The Fannie Mae Q2 2026 Special Topic Report evaluated which factors were most likely to boost home sales during the spring home-buying season and which would hurt sales.

The top influences that would encourage people to buy homes were households formed by millennial and Gen Z families, inventory of houses for sale, and household budgets and wealth, according to the survey.

More on home sales and the housing market:

- Zillow discovers changes in mortgage rates, housing market

- Realtors group flags ‘mismatch’ squeezing middle-class homebuyers

- Americans face decision after unexpected housing market news

The factors most likely to hurt home sales was home prices/affordability. Consumer confidence and sentiment was second, and mortgage rate levels came in at third.

This third factor is certainly understandable, since Freddie Mac mortgage rates have been mostly increasing since late April. Home loan rates may decrease here and there, but Fannie Mae expects rates to stay above 6% throughout 2026 and 2027.

Key takeaways from Fannie Mae’s data

It can be difficult to decipher reports that are mostly just numbers and percentages. Here’s what the latest predictions from the Fannie Mae Home Price Expectations Survey (HPES) means for homebuyers, sellers, and owners.

- Buyers can expect prices to keep increasing. Housing costs generally increase over time. However, the market is more homebuyer-friendly than it was during the peak of the COVID-19 pandemic, so inclines won’t be nearly as intense as they were a few years ago.

- Sellers should be strategic about pricing. You can’t list your home like it’s 2022 anymore, because housing prices aren’t soaring anymore. You need to set a realistic listing price, otherwise you risk leaving your home on the market for a long time and possibly cutting the price later.

- Owners will build home equity more gradually. Homeowners build equity in two ways: paying down their mortgage principal and allowing their home to increase in value. Expect your property to continue gaining value, just more moderately than in the early 2020s.

- High mortgage rates are still affecting homebuyers. Not only were high rates the third-strongest hindrance to home sales in Fannie Mae’s Special Topics Report, but the rate lock-in effect was in fourth place. People are staying in their homes because they locked in super-low interest rates during the pandemic. So, potential buyers are hesitant to buy because they don’t want to take on a high rate, and homeowners are hesitant to sell because they don’t want to lose their low rate.