The contentious clash of divergent opinions on the Federal Reserve’s outlook on short-term interest rates has clarified with three regional bank presidents zeroing in on increasing uncertainty about the Iran war’s impact on inflation.

Fed watchers agree that the hawkish tea leaves spilling out of the central bank’s April 28-29 meeting indicate the dissenters do not believe it was appropriate for the Federal Open Market Committee to signal that the next interest rate action could be to lower rates.

Judging from the language in its official post-meeting statement, the FOMC appears to signal it could cut benchmark interest rates this year — rates that guide short-term borrowing from credit cards to business loans, and even indirectly, mortgage rates in the stagnant U.S. housing market.

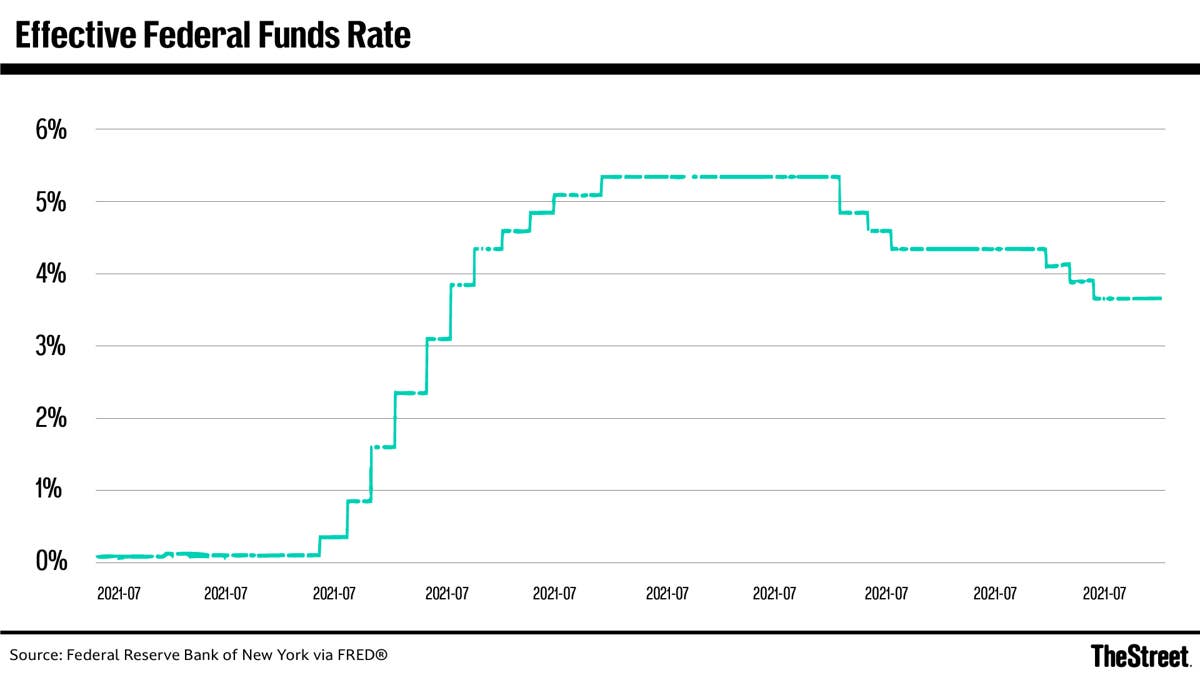

The FOMC, in a decisive 8-4 vote on April 29, held the benchmark federal funds rate steady at 3.50% to 3.75%.

The primary point of three of the opposing votes? The two magic words “additional adjustments,” which in Fed-speak means, in this situation, a signaling of resumption of rate cuts.

Regional presidents Beth Hammack of Cleveland, Neel Kashkari of Minneapolis, and Lorie Logan of Dallas all released independent statements May 1, saying the Fed should be more explicit that the next monetary-policy step may not be a rate cut, but rather a rate hike as inflation risks rise due to the Iran war.

“I believe the FOMC should offer a policy outlook that signals that the next rate change could be either a cut or a hike, depending on how the economy evolves,” Kashkari said in a statement released May 1.

“This could tighten financial conditions somewhat today, pushing back against a high-inflation scenario that could require an even stronger monetary policy response in the future,’’ Kashkari said.

Historic FOMC vote reflects 8-4 divide

It was the FOMC’s third pause after making three quarter-point cuts during its last three meetings of 2025 due to a weakening labor market — and the first time in more than 30 years the FOMC vote reflected four dissents.

“The center is moving toward a more neutral place,” outgoing Fed Chair Jerome Powelltold the post-meeting press conference, describing the U.S. economy as “resilient” in spite of the decade’s price shocks from the Ukraine and Iran wars, the Covid pandemic, and President Donald Trump’s tariffs.

A neutral state is when an economy operates at sustainable growth with stable inflation and full employment without overheating or recessionary pressure.

It can also mean interest rates move in either direction.

But Powell added: “People are not saying that we need to hike now.”

FOMC rate outlook divides voting Fed officials

The FOMC statement said that “developments in the Middle East are contributing to a high level of uncertainty about the economic outlook.”

“In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook and the balance of risks,’’ the statement said.

Fed Governor Stephen I. Miran voted against the rate pause, preferring to lower the target range for the funds rate by a quarter-point.

Miran, the most dovish of the Board of Governors, will be replaced by incoming Fed Chair Kevin Warsh later this spring.

Hammock cites risk of economic uncertainty changing rate outlook

In general, Kashkari, Logan, and Hammack concurred with the rate pause but not with the signal that the next policy move would be to resume lowering interest rates.

In a separate statement published May 1, Hammack agreed with Powell that the economy has been resilient so far this year but added that rising oil prices add to broad-based inflationary pressures.

The current FOMC statement references language around “additional adjustments” reflecting forward guidance put into the statement to signal a pause rather than an end to the easing cycle, she said.

“Uncertainty around the economic outlook has increased in 2026 and makes the future path for monetary policy more uncertain, as well,” she said. “I see this clear easing bias as no longer appropriate given the outlook.”

Logan cites impact of Iran war on U.S. inflationary pressures

The Fed’s dual mandate from Congress requires maximum employment and stable prices.

- Lower interest rates support hiring but can fuel inflation. This risks fueling further inflation, potentially leading to an inflationary spiral.

- Higher rates cool prices but can weaken the job market. This increases the cost of borrowing and further stifles economic activity.

The eight-week Iraq war raises the prospect of prolonged or repeated supply disruptions that could create further inflationary pressures. At the same time, the labor market has been stable, with low unemployment and payroll job gains keeping pace with labor force growth, Logan said in her May 1 statement.

Related: Fed drops rate-cut bombshell

When the FOMC gives forward guidance about the likely course of future interest rates, as in the recent post-meeting statement, that guidance is an important policy tool, she said, adding that households and businesses rely on the guidance to make future plans.

“When the FOMC gives forward guidance, it is important for that guidance to reflect the policy outlook,’’ Logan said. “In light of the two-sided risks to monetary policy, I believed the FOMC should not give forward guidance implying a bias toward rate cuts at this time.”

Investors outline future interest-rate path

Traders are currently pricing in the next interest-rate cut for mid-to-late 2027, according to the CME FedWatch Tool.

The Kalshi prediction market estimates a 43% chance of a Fed rate hike before July 2027.

Vinny Amaru, global investment strategist at J.P. Morgan Wealth Management, said in an email to TheStreet that the details coming out of the FOMC meeting were “interesting.”

“With the labor market showing some signs of stabilizing and higher oil prices contributing to elevated inflation, we see the Federal Reserve holding rates steady for the rest of the year,’’ he said.

Tony Welch, chief investment officer at SignatureFD, told TheStreet in an email that the multiple dissents are “something important: the Fed is no longer fully aligned on what comes next.”

“The economy is holding up, supported by consumer spending and investment, but inflation remains sticky,” he said. “That combination reinforces a Fed that we believe is likely to stay on hold for longer than many expected.”

The next FOMC meeting is June 16-17.

Related: BNP Paribas flags rate outlook after divisive Fed vote