Young couples who welcome their first child often focus on diapers, daycare and sleepless nights. But they also face a new financial reality: They now have someone who depends on them financially and legally.

In this interview, Harry Margolis, author of Get Your Ducks in a Row, discusses the estate planning steps new parents should consider, including naming guardians, setting up trusts and purchasing life insurance.

Below is a transcript of the interview with Margolis, edited for brevity and clarity.

Why having a child changes everything

Robert Powell: So many young couples who have their firstborn are at a loss trying to figure out what to do next from an estate planning perspective. Where should they begin?

Harry Margolis:This is probably one of the two classic times that people do estate planning – when they have a child and when they retire.

There’s usually a pretty big gap between those two periods when people probably should revisit their estate plans, but most don’t.

The real issue when you have a child is that you now have a dependent, someone you’re responsible for. Hopefully, in most cases, parents will be around and it won’t become an issue. But what happens if they’re not?

Naming guardians and trustees

Harry Margolis: You need to do a couple of things.

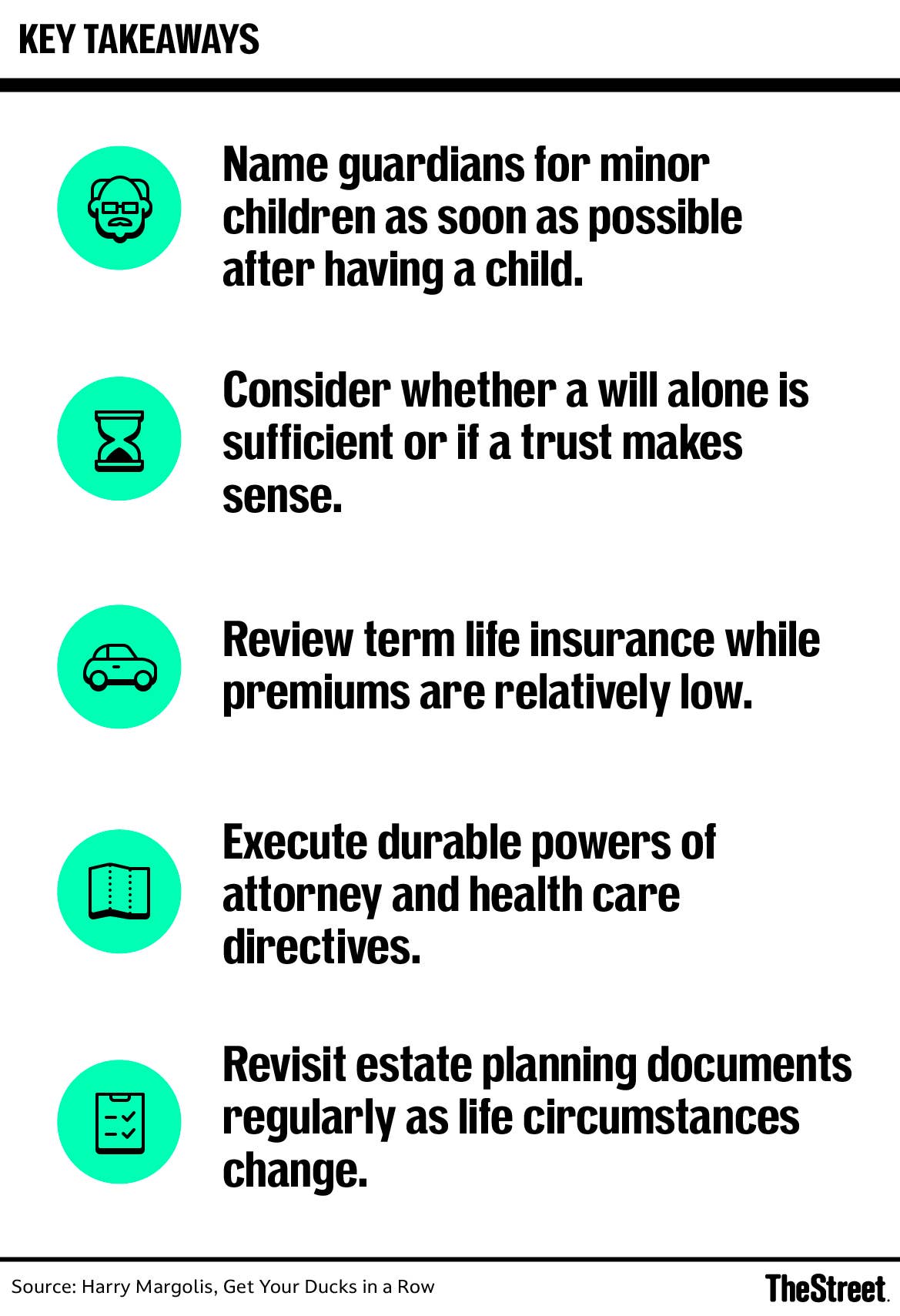

First, you need to name a guardian, or guardians, to step in if you and your spouse or partner aren’t around. That can be a difficult choice because no one is going to be exactly the same as the parents.

In some cases, it’s obvious who it should be. In others, it’s difficult. But you should make the choice so it’s clear. You do that in your will.

In your will, you name who will be guardian for your children. In most states, you can also use a side document to name a temporary guardian in case you’re disabled for a period of time.

Then there’s the question of who’s going to manage the money you leave behind.

The simplest thing, especially for younger families that may not have significant assets yet, is to include a provision in your will naming a trustee to manage the funds for your child or children.

If you have more assets, you might want a separate trust so you can be more flexible about the terms – when children receive the money and under what conditions.

Those are probably the most important things.

Why life insurance matters for young families

Harry Margolis: The other thing, which is less an estate planning issue, is buying life insurance.

If you’re younger, you probably don’t have a lot of assets yet. But you want to leave something for your children or your spouse in case you’re not there.

That can be very important. If you buy term life insurance while you’re younger and in good health, it’s usually pretty inexpensive.

That may actually be more important than the estate planning itself.

The estate planning documents every adult needs

Harry Margolis: There are also standard estate planning documents that everybody should execute, including a durable power of attorney and a health care proxy or health care directive.

Why many families wait too long

Robert Powell: In your experience – and I know you’ve practiced elder law for much of your career – do you find parents overlook this, or are they generally on top of it?

Harry Margolis: The people who come to me are obviously on top of it, so that’s part of it. I don’t really have a good group to comment on more broadly.

But the bulk of our practice involves the other group I mentioned earlier – people doing estate planning around retirement because so many baby boomers are at that stage now.

A lot of them have documents they executed 40 years earlier that are now totally out of date.

So I do think many people handle estate planning when they have children, but they often don’t revisit those documents later.