Retirees may want to think twice before automatically harvesting investment losses.

Or at least so said Jeffrey Levine, chief planning officer at Focus Partners Wealth, in a recent episode of Focus on Finance Forum.

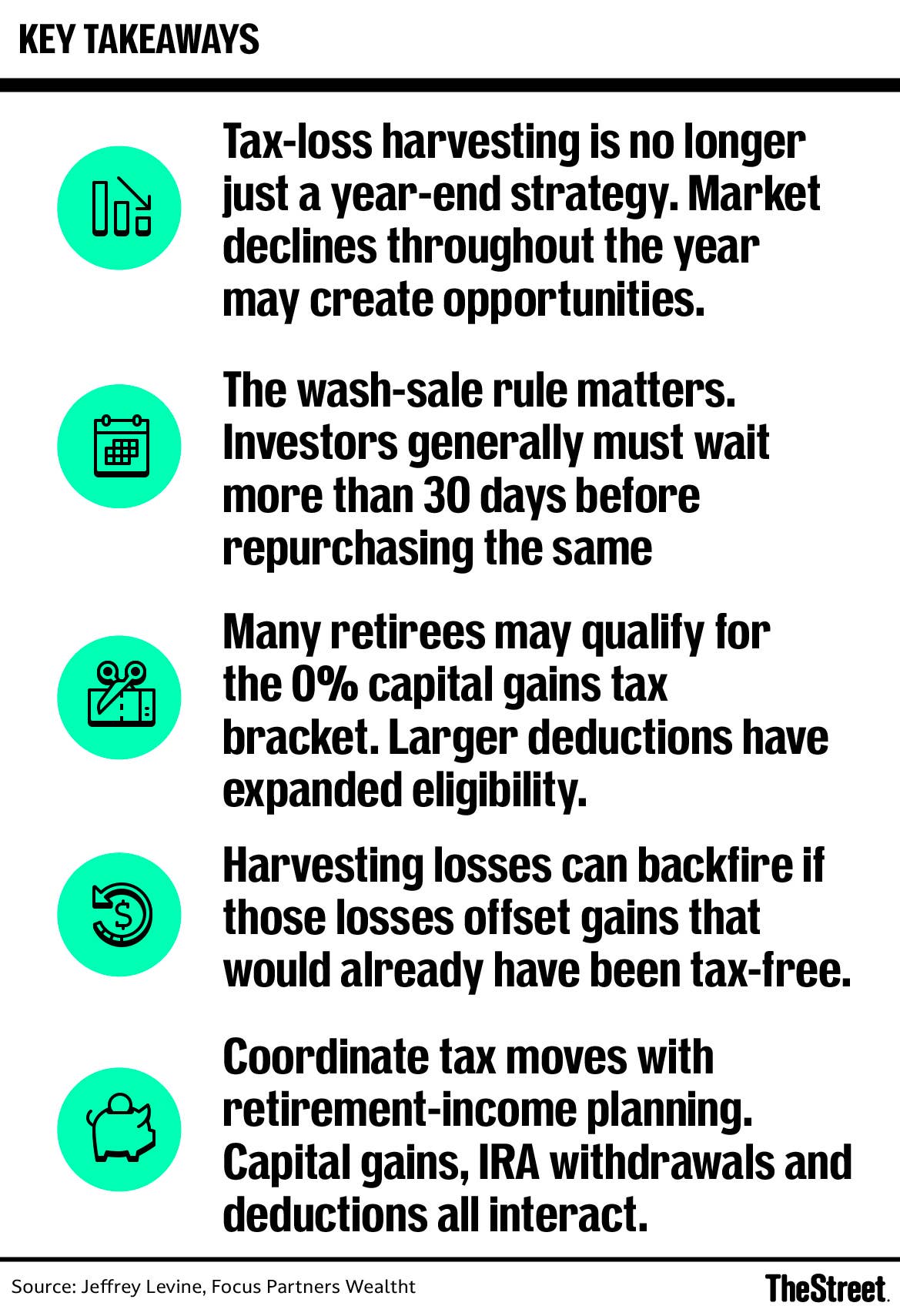

In the episode, Levine explored why tax-loss harvesting is no longer just a year-end planning strategy, how losses can create future tax flexibility and why more retirees may qualify for the 0% long-term capital gains bracket because of larger deductions available under current law.

Below is a transcript of the interview with Levine, edited for brevity and clarity.

Why tax-loss harvesting matters year-round

Jeffrey Levine: A lot of people think about tax-loss harvesting in the context of year-end planning. But while it should be considered as part of year-end planning, it’s also something you can do on a regular and ongoing basis.

Let’s say you have an investment worth $100,000 on Jan. 1. By mid-January, maybe after a rough couple of weeks, it’s worth $90,000. If you don’t do anything, there’s a possibility that by February or March it recovers and moves back above where it started.

If that $100,000 investment drops to $90,000, you can sell it and claim the loss. You can’t buy it back immediately because of the wash-sale rule. You have to wait more than 30 days before repurchasing it in order to claim the loss.

The point is that if you sit on your hands, you may lose the opportunity to use that loss. Losses can be very valuable from a tax standpoint.

The trade-off between losses and market recovery

Levine: Economically, nobody wants losses. I hope your investments don’t lose money. But if something has gone down in value, you want to make the most of it.

The challenge is deciding whether you want the loss badly enough to risk sitting out of the investment for 30 days.

You’d be disappointed if your investment fell from $100,000 to $90,000, you sold it, and then during the next 30 days it bounced back to $105,000 before you could buy it again. In that case, you captured a $10,000 loss but missed a $15,000 recovery in gains.

That’s why some investors don’t sit in cash after selling. They may buy something similar, but not too similar, to avoid violating the wash-sale rule.

Robert Powell: You also don’t do this in a vacuum. Maybe you’ve got unrealized capital gains elsewhere in your portfolio. Banking capital losses could help offset gains you realize later in the year.

Maybe you bought something for $100 that’s now worth $200 and want to take some profits. Having capital losses available to offset those gains may not be a bad strategy.

How capital losses offset gains and income

Levine: That’s exactly right. Losses create optionality without an immediate tax impact.

A lot of investors hesitate to rebalance or trim concentrated stock positions because they don’t want to pay taxes. Banking losses along the way can allow you to sell appreciated investments later without triggering taxes.

Here’s how it works at a basic level. Capital losses offset capital gains. There are long-term and short-term netting rules, but the big takeaway is simple: losses can offset gains.

If you have more losses than gains, you can use up to $3,000 of remaining losses to offset ordinary income each year.

For example, suppose you have $50,000 of losses and $20,000 of gains. Your losses first offset the gains, leaving you with $30,000 of net losses.

You pay no tax on the gains. Then you can use $3,000 of the remaining losses to offset other income, such as wages, interest, dividends or IRA distributions.

The remaining $27,000 isn’t lost. It carries forward into future years.

If you regularly review your portfolio and harvest losses when appropriate, you may gradually build a bank of losses that can offset future gains.

When harvesting losses may backfire

Powell: When you think about the possibility that someone could pay 0% taxes on long-term capital gains, does that factor into the equation?

Levine: Absolutely. That’s one of the reasons not to harvest losses.

Paying 0% tax is the best possible outcome. In fact, paying 0% is better than simply deferring taxes.

If you bought something for $10,000 and it grows to $30,000 but you never sell it, you haven’t paid taxes yet, but you may owe taxes eventually.

If you sell it while you’re in the 0% long-term capital gains bracket, that gain becomes permanently tax-free.

So yes, there are situations where harvesting losses may not make sense.

Why retirees may qualify for the 0% capital gains rate

Levine: More people than ever may qualify for the 0% long-term capital gains bracket, especially retirees.

For 2026, the standard deduction is more than $30,000 for married couples. People over 65 also receive additional standard deductions. On top of that, enhanced senior deductions created under the One Big Beautiful Bill Act add another $6,000 per person.

A married couple over 65 could easily have more than $45,000 of deductions before itemizing anything else.

You need close to $100,000 of taxable income before leaving the 0% long-term capital gains bracket. So many married couples over 65 with total income under roughly $140,000 may still qualify for the 0% rate.

Powell: That’s a livable income for many retirees.

If someone harvests losses early in the year and later discovers they qualify for the 0% capital gains bracket, can they carry the losses forward instead of using them immediately?

Levine: No. The losses first offset capital gains automatically.

Using our earlier example, if you had $50,000 of losses and $20,000 of gains, those losses would first offset the gains, even if the gains would otherwise have been taxed at 0%.

You don’t get to choose to preserve the losses for later.

Like most tax planning questions, the answer is: it depends. Whether tax-loss harvesting makes sense depends on your individual situation.